In the high-stakes world of PR and digital marketing, agility is often the only competitive advantage that remains. When a trend breaks on social media or a client needs an emergency ad-spend pivot, the old guard of agency finance, centralised credit cards and manual reimbursement forms, becomes a significant bottleneck that no amount of talent or strategy can work around.

For modern agency leaders, the goal is no longer just “budgeting”; it’s Financial RevOps. This means putting the power to execute directly into the hands of your department heads, while maintaining full visibility and oversight at the leadership level. To get there, agencies are moving away from traditional corporate banking and toward a distributed spending model that matches the speed at which the best creative work actually happens.

The managerial gap in new ventures

In the early stages of a B2B marketing venture or a boutique PR shop, the founder often plays the role of CEO, Account Manager, and CFO simultaneously. As you scale, however, this founder-as-gatekeeper model leads to burnout and operational stagnation, because every spending decision, no matter how small, has to route through one person before anything can move.

To transition from a hustle to a firm, you need specialised managers who own specific parts of the financial workflow rather than waiting for permission to do their jobs:

- The RevOps Manager: bridges the gap between sales and finance, ensuring that tools like HubSpot or SEMrush are paid for, renewed on time, and actually utilised effectively across the team.

- The Procurement Lead: manages the dozens of small, recurring SaaS subscriptions that power a modern agency, from media monitoring platforms to design tools to distribution services.

- The External Financial Advisor: a fractional CFO who helps you transition from surviving month-to-month to building the financial infrastructure needed for sustainable, scalable growth.

Distributed spending: powering the procurement lead

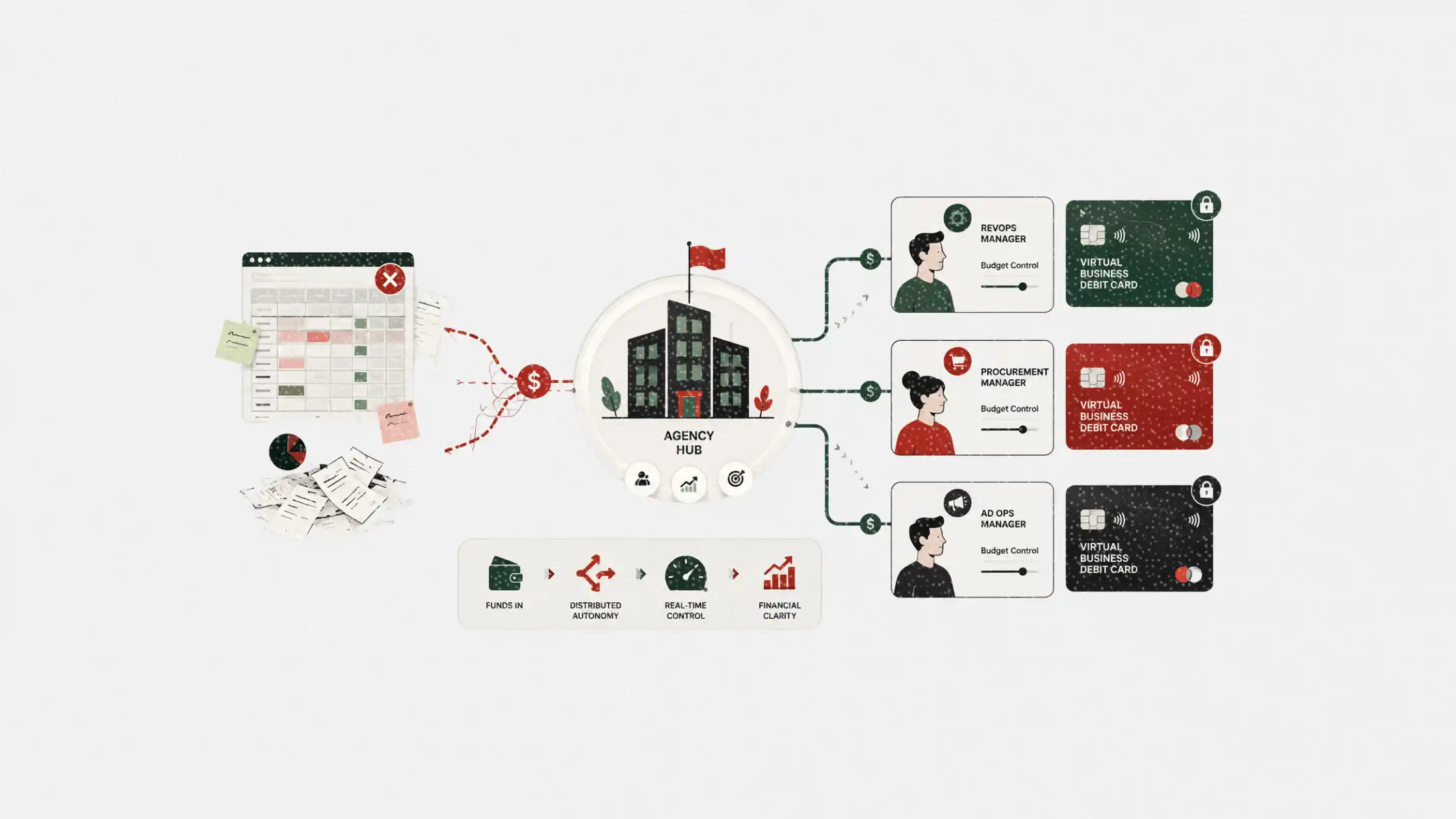

The most effective way to empower these managers is to decouple agency spending from the founder’s personal or primary business card. This is where modern digital banking solves a classic agency pain point cleanly and without the overhead of traditional corporate account structures.

The most effective way to empower these managers is to decouple agency spending from the founder’s personal or primary business card. For many agency operators, the starting point is simply to sign up for a debit card online tied to a dedicated business account, one that allows them to issue virtual, project-specific cards and put the right budget in the right hands instantly. In practice, that looks like this:

- For the PR Manager: a card capped at $500 per month specifically for wire distribution services and media databases, so campaign execution never stalls waiting for approval on a $40 charge.

- For the Ad Ops Team: dedicated virtual cards for Meta or LinkedIn ads, ensuring that a personal spending limit never accidentally pauses a client’s high-stakes campaign at a critical moment.

- For the Office Manager: a controlled card for the culture budget, covering team lunches, software for a new hire, or emergency hardware, with full visibility into how that budget is being used.

This is the practical meaning of agile procurement: the right person has the right tool, with the right limit, before they need it.

Why debit-first wins for agency stability

While many agencies lean on credit for rewards points and float, the debit-first approach is becoming the preferred strategy for lean, AI-driven agencies that prioritise margin clarity over perks. It offers three distinct advantages worth building into your financial model:

- Zero interest, zero debt: you are spending real-time revenue, which means your agency’s profit margins are not being quietly eroded by compounding interest on operational expenses.

- Instant accountability: most digital-first business accounts offer real-time transaction tagging, so the moment a manager makes a purchase, the expense is categorised by client or department without any manual reconciliation at the end of the month.

- Risk mitigation: if a subscription service is compromised or a virtual card needs to be cancelled, you only lose what is allocated to that specific card, not your entire agency line of credit.

For agencies managing multiple client budgets simultaneously, that third point alone is worth the switch.

Conclusion

Budgeting in the current media landscape is not about restriction; it is about enablement. Distributed spending models, supported by digital-first business banking and the ability to get a debit card online for each department or project, shift the agency from a centralised, slow-moving hierarchy to an autonomous operation where managers can act on their expertise without a 48-hour approval chain standing in the way.

Your team does not need more meetings to discuss whether a $50 stock photo purchase is justified. They need financial infrastructure that matches the pace of the work, so the agency’s energy goes into storytelling and client results rather than chasing down receipts and waiting on sign-offs.

The agencies that build this way now will be structurally faster than those that don’t, and in a business where speed and creative momentum are everything, that gap compounds quickly.

FAQs

What is a distributed spending model for agencies? A distributed spending model gives individual managers or departments their own dedicated payment cards with preset limits, rather than routing all purchases through a single centralised account or founder card. It maintains oversight at the leadership level while removing approval bottlenecks at the execution level.

How is a virtual business debit card different from a standard corporate card? A virtual business debit card is a digital card issued instantly, tied to a specific budget or project, and usable for online purchases immediately. Unlike a standard corporate card, it can be capped, cancelled, or reassigned without affecting the rest of the agency’s payment infrastructure.

What should agencies look for when choosing a digital banking platform? Prioritise platforms that offer virtual card issuance, real-time transaction categorisation, integrations with accounting tools like Xero or QuickBooks, and granular spending controls per card. Low or no foreign transaction fees are also worth checking if your agency works with international vendors or media platforms.

When is the right time for an agency to move to a distributed spending model? The clearest signal is when the founder or finance lead is regularly being pulled into small spending approvals that have nothing to do with strategy. If operational purchases are creating delays on billable work, the infrastructure has already fallen behind the pace of the business.

Is a debit-first approach suitable for agencies with fluctuating cash flow? It works best when paired with a healthy operating reserve, typically one to two months of fixed costs sitting in the business account at all times. With that buffer in place, a debit-first model actually improves cash flow visibility because every spend is a real-time reflection of what the business has, not what it can borrow.

Leave a Reply