The creator economy is consolidating fast. Platforms are being absorbed by holding companies, commerce infrastructure is attracting premium valuations, and new tools are raising seed rounds with a different thesis than the generation before. For brand marketers, tracking this deal flow directly affects which platforms remain independent, how pricing shifts, and whether the tools you rely on today will look the same next year.

Table of contents

Jump to each section:

- Why M&A in the creator economy matters to brand marketers

- The landmark 2025 deals shaping the current market

- Funding and acquisitions in 2026 so far

- What this consolidation wave means for your program

Why M&A in the creator economy matters to brand marketers

When a platform gets acquired, pricing tends to shift toward the acquirer’s client base, feature roadmaps change to serve the parent company’s priorities, and creator rosters may move. None of that is necessarily bad, but it affects any brand that built a workflow around the acquired platform.

According to the Quartermast Advisors 2026 Creator Economy M&A Report, 81 creator economy deals closed in 2025, a 17.4% increase from 69 in 2024. Software businesses led all acquisition categories at 25.9% of deals, followed by agencies at 21%, media properties at 16%, and talent management firms at 14%.

The landmark 2025 deals shaping the current market

Two 2025 acquisitions have reset the competitive landscape heading into this year.

Later’s purchase of Mavely from Nu Skin Enterprises for US$250 million in January 2025 merged a tech-enabled affiliate commerce platform into Later’s creator management infrastructure. The combined entity now runs across 16 million analyzed creators with more than US$2 billion in verified influencer-driven purchases annually.

Publicis Groupe’s acquisition of Captiv8 for US$175 million in May 2025 completed a two-year buying spree. Captiv8, operating a network of 15 million creators across 120 countries, added affiliate discovery and shoppable content capabilities to the stack Publicis already held through its 2024 purchase of Influential for US$500 million.

The combined Publicis platform now connects creator strategy, paid activation, and cross-channel measurement at an enterprise scale few independent tools can match.

ShopMy raised US$70 million at a US$1.5 billion valuation in October 2025, led by Avenir with participation from Bain Capital Ventures and Bessemer Venture Partners. The platform connected premium brands to over 185,000 creators for affiliate commerce, reached profitability in 2024, and posted 200% revenue growth year-on-year.

The valuation reflects what defensible creator commerce infrastructure commands when discovery, attribution, and creator monetization are solved in a single system.

Funding and acquisitions in 2026 so far

New capital in 2026 has been more selective. One estimate put creator economy venture funding in the first five months of 2026 at roughly US$58 million across nine deals, compared with approximately US$807 million across eleven deals in the same 2025 period. Strategic acquisition activity has continued regardless.

Devotion, co-founded by Cami Tellez (previously of Parade) and former TikTok executive Jon Kroopf, raised US$4 million in a seed round led by Basecase and Will Ventures in March 2026. The platform manages high-scale creator ecosystems for enterprise brands, handling content vetting against brand guidelines, brand fit scoring, and creator payments. Tellez’s thesis: brands need to operate as content networks, managing hundreds of creators simultaneously.

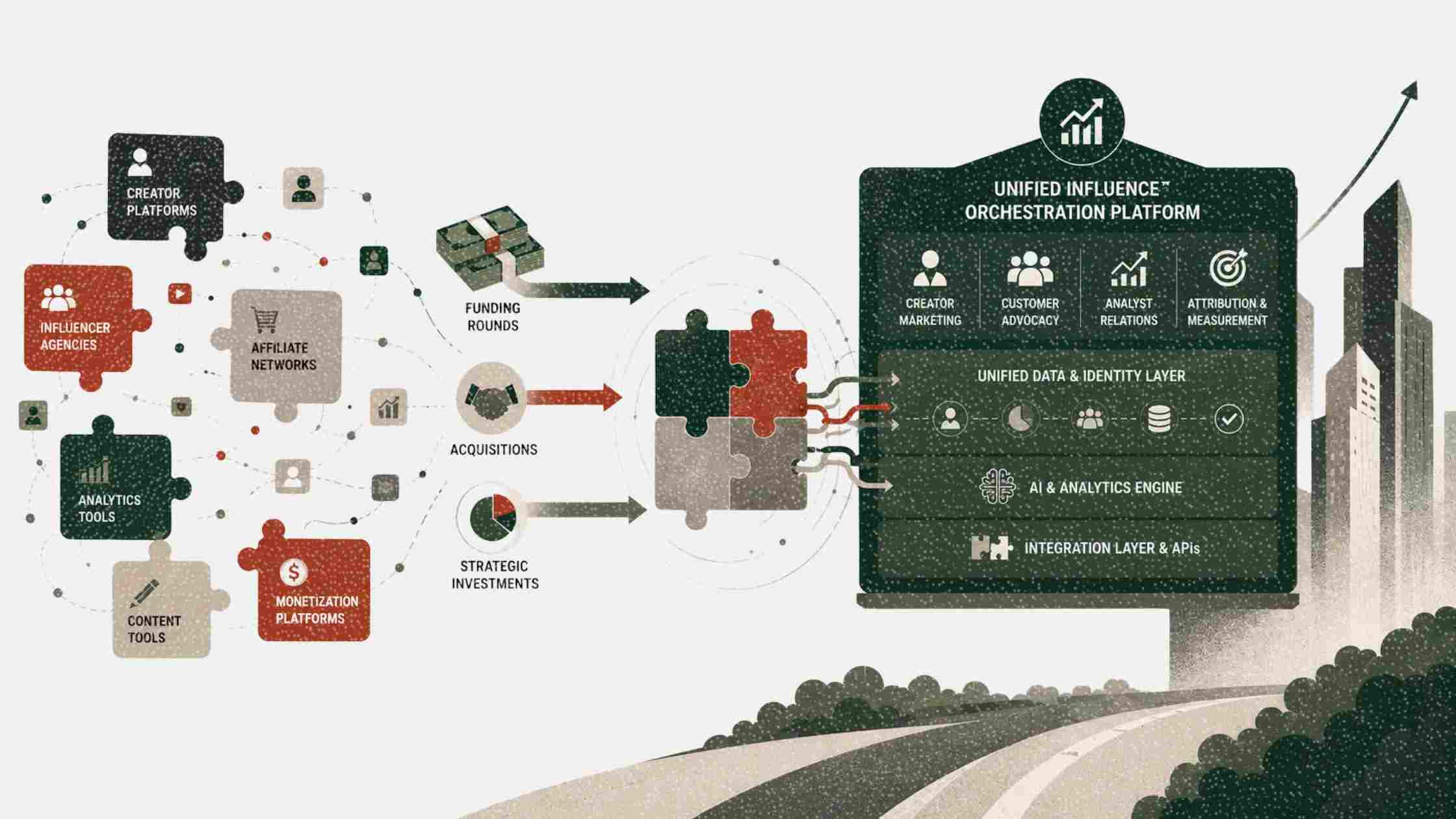

The most B2B-relevant deal of the year so far is Spotlight’s acquisition of Captivate Collective in February 2026. Spotlight, backed by Stone-Goff Partners, combined its analyst relations capabilities with Captivate’s customer marketing and advocacy programs to create what both companies describe as the market’s first end-to-end Influence Orchestration platform for B2B organizations.

The deal addresses the fragmented influence programs most B2B teams run, with analyst relations, customer advocacy, and creator programs managed as separate functions with no shared measurement.

Dinda Anandita, Account Director at content-led comms agency Content Collision, flags the Spotlight deal as a signal for B2B teams still operating in silos: “The brands that benefit from consolidation are the ones who have already mapped how analyst credibility, customer advocacy, and creator reach connect in their buyer journey. If those three things still sit in separate budgets with no shared measurement, the emerging integrated platforms will not fix the problem automatically. The infrastructure is only as useful as the strategic brief behind it.”

What this consolidation wave means for your program

Three implications follow. First, include acquisition trajectory in your platform evaluations. An independent platform acquired by a large holding company may reprice toward enterprise within twelve to eighteen months.

Second, affiliate and commerce attribution infrastructure is the category attracting the most capital, and for a clear reason: it connects creator activity to verified transactions. If your current stack does not do that, the platforms commanding premium valuations increasingly represent the new baseline expectation

Third, the Spotlight-Captivate Collective deal signals that B2B influence infrastructure is maturing into a distinct category, separate from B2C creator marketing.

Leave a Reply